“CUDIC has outgrown legacy legislation and FICOM’s shadow. CUDIC is responsible for deposit insurance of a C$77 billion industry that is used by almost half of British Columbians. Larger than most Canadian credit unions then it warrants full-time, permanent executive leadership. Larger than most B.C. Crown Corporations then it deserves independent, empowered and accountable governance oversight.”

CONTEXT

The following submission was authored by Ross McDonald, in a personal capacity, in response to the Second Public Consultation Paper of a legislative review by the Ministry of Finance of the B.C. provincial government. Under the review, the Ministry of Finance sought public submissions by 19 June 2018. The legislative review considers changes to the Financial Institutions Act and the Credit Union Incorporation Act. This submission provides four recommendations on a targeted subset of relevant topics. Recommendations per this submission are aligned with stated legislative objective and collectively offer policy ideas that have the potential to courageously transform the regulatory environment of B.C. credit unions for the benefit of industry, government, taxpayers and employees.

Ross wishes to thank various credit union system veterans that kindly volunteered leadership inspiration, technical insight and professional encouragement. Thank you, appreciated.

This submission may be easier to read in PDF format. Download per bit.ly/fia-cuia-rm-pdf

EXECUTIVE SUMMARY

This personal submission to the FIA/CUIA Review seeks to frame an alternative regulatory structure for B.C. credit unions. Specifically, the submission provides four recommendations:

Recommendation 1 - Roles & Responsibilities

Transfer the mandate for prudential supervision, including completion of risk-based assessments and determination of deposit insurance premiums, of B.C. credit unions and credit union centrals from FICOM to CUDIC. Terminate any requirement that CUDIC be administered by FICOM.

Recommendation 2 - Legal Entities

Establish CUDIC as a Crown agency. Retain FICOM as branch of the Ministry of Finance. Collaborate with industry to review the legislative mandate, appropriate sustainable resources, and any potential merger of Stabilization Central Credit Union.

Recommendation 3 - Leadership & Governance

Appoint permanent executive and an independent, empowered governance body to provide leadership and oversight of CUDIC. Related competency matrices and governance processes should reflect CUDIC financial size, technical complexity and systemic role. CUDIC Board should adopt, and strive for excellence in, relevant governance best practices.

Recommendation 4 - Public Accountability

Regardless of their legal entity structure then FICOM and CUDIC should, as separate organizations, be subject to the “Performance Reporting Principles” and “Taxpayer Accountability Principles” as published by the B.C. government.

The recommendations are aligned with the primary objective of the legislative and regulatory framework “to maintain stability and confidence in the financial services sector by reducing the risk of failures and providing consumer protection and supporting objectives.” Related execution would necessitate short-term legislative change and organizational restructuring. Some portion of this work may be already actively engaged given the initial recommendations by the B.C. Ministry of Finance.

The recommendations recognize the current size, elevated complexity, resource challenges and peer jurisdiction approaches in regards regulatory oversight of credit unions. Recommendations may create significant benefits to government, to industry and to the public over a medium-term basis. Given numerous, diverse and substantive externalities that face the credit union industry, the recommendations may position the regulatory oversight for the coming decade until the next legislative review.

The author believes that credit unions contribute materially to the economy, employment and communities of B.C. This submission is motivated by personal appetite for a strong and sustainable B.C. credit union industry; for an effective, efficient and appropriate regulatory structure; for best practice adoption in regards governance oversight and public accountability.

RECOMMENDATION 1 - ROLES & RESPONSIBILITIES

Recommendation: Transfer the mandate for prudential supervision, including completion of risk-based assessments and determination of deposit insurance premiums, of B.C. credit unions and credit union centrals from FICOM to CUDIC. Terminate any requirement that CUDIC be administered by FICOM.

B.C. has the largest provincial credit union system in Canada. As at 31 December 2017 then B.C. credit unions reported C$77 billion of assets, C$66 billion of member deposits and 2.0 million members that represent over two-fifths of the provincial population. Three of the top five Canadian credit unions are located in British Columbia. The B.C. credit industry is growing. Between 2005 and 2017, B.C. credit union assets increased from C$36 to C$77 billion and membership increased from 1.5 to 2.0 million.

Over recent years, credit union operations have increased in complexity. Elevated consumer expectations, heightened competition and evolving technological innovation have necessitated significant investment by credit union organizations in digital channels, product offerings and operational efficiency. Increased scale may have permitted increased sophistication by larger B.C. credit unions. For example, between December 2007 and 2017, the total assets of Vancity Credit Union increased from C$14.1 to C$21.7 billion (Source: Vancity CU).

The B.C. credit union industry and its regulator gained national, systemic impact. In recognition of its importance to Canadian credit unions then, in 2014, FICOM designated Central 1 Credit Union as a Domestically Systemically Important Financial Institution. As such, it subject to commensurately elevated regulatory requirements and prudential supervisory expectations. Between 2005 and 2017, Central 1 Credit Union assets increased from C$5 to C$18 billion. While asset growth includes a 2008 merger with Credit Union Central of Ontario then the majority of asset growth was driven by higher member deposits at B.C. credit unions. As of 1 January 2017, responsibility for regulatory oversight of Central 1 Credit Union passed from the federal Office of the Superintendent of Financial Institutions to FICOM. Central 1 Credit Union holds mandatory liquidity deposits for all B.C. and some ON credit unions. It provides wholesale payments, treasury and numerous other services to credit unions nationwide. The nature and complexity of its operations, and therefore its regulatory policies and prudential supervisory approach, are materially different from that of a credit union.

FICOM does not appear to have the operational capabilities to fulfil its mandate in regards credit union prudential supervision. In 2016, the BC Auditor General concluded that “FICOM may not be able to detect a worsening situation at a credit union in time to address and reduce the risk of failure.” This expert, independent determination strikes at the heart of the prudential supervision function. FICOM Supervisory Framework publication states that “the objective of FICOM’s supervision is to reduce the likelihood that a provincially regulated financial institution will fail.”

Over recent years, FICOM appears to have completed a very small number of supervisory reviews of credit unions. B.C. has 42 credit unions. The 2014 BC Auditor General report stated that “With their shortage of staff, it would take over 14 years to review all of BC’s credit unions instead of FICOM’s intended target of two to three”. It could be inferred that FICOM completed supervisory reviews of three credit unions (42 divided by 14), or equivalents thereof, each year. This compares to the 14 to 21 credit unions, or equivalents, that require prudential supervisory reviews annually to achieve FICOM’s target. The 2016 BC Auditor General report stated that “FICOM’s actions to address its staffing shortage are not working. FICOM has further reduced the number of credit union reviews it will do each year”. This suggests that FICOM prudential supervision team may review each credit union once every couple of decades or so. This frequency of review compares extremely poorly to regulatory standards in other jurisdictions and in other regulated industries. The lack of timely supervisory assessments of credit unions may increase deposit insurance risks for B.C. taxpayers, given current unlimited deposit insurance policy.

“FICOM may not be able to detect a worsening situation at a credit union in time to address the risk of failure.”

The extent of FICOM’s responsibilities are materially greater than those of peer provincial regulatory entities. FICOM regulates multiple industries - credit unions, trust companies, insurance companies, real estate, mortgage brokers, strata properties and pension plans. FICOM performs substantially all regulatory function for B.C. credit unions. Specifically FICOM - inclusive of CUDIC - is responsible for regulatory policy, statutory approvals, prudential supervision, deposit insurance and market conduct. Most, if not all, other Canadian provincial regulatory structures use multiple organizations to perform equivalent industry coverage and functional responsibilities.

Despite FICOM’s multi-year resource challenges, its authority was recently further extended. In 2017, the BC Ministry of Finance tasked FICOM with the new function of Office of the Superintendent of Real Estate, a seemingly prominent and impactful role given the substantive recommendations of the B.C. Government’s Independent Advisory Group.

The B.C. Ministry of Finance should revisit any business case that requires CUDIC to outsource its administration and/or operations to FICOM. The BC Ministry of Finance FIA/CUIA March 2018 recommendations state that “CUDIC was merged with FICOM in 1990 to allow expertise to be pooled; that pooling of expertise continues to be relevant and important today.” At that time then both FICOM and CUDIC were startup organizations, perhaps with an all-hands-on-deck mindset. But CUDIC and FICOM are now mature organizations. The rationale of pooled expertise between FICOM and CUDIC may reflect legacy pragmatism rather than current circumstances or future needs of the B.C. credit union industry and related regulation.

FICOM operational capabilities to set regulatory policy for credit unions appear effective under the current organizational structure. Since the prior FIA/CUIA review then FICOM has introduced, and updated, a significant number of regulatory guidelines. It has also progressed multiple adhoc initiatives, such as stress tests, in efforts to assess industry risk and/or to enhance credit union capabilities.

RECOMMENDATION 2 - LEGAL ENTITIES

Recommendation: Establish CUDIC as a Crown agency. Retain FICOM as branch of the Ministry of Finance. Collaborate with industry to review the legislative mandate, appropriate sustainable resources, and any potential merger of Stabilization Central Credit Union.

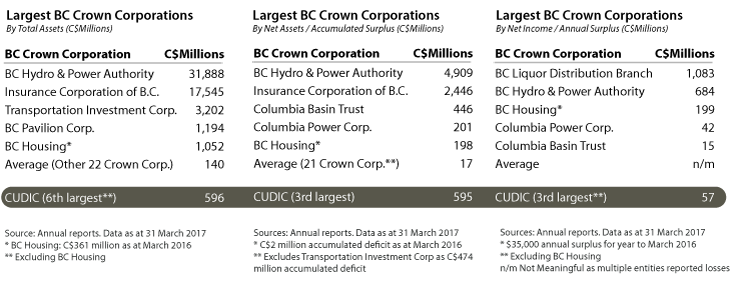

The size of CUDIC net income may warrant it being a standalone organization. For the year to March 2017, CUDIC net income of C$57 million. Such earnings are large relative to a) BC’s largest credit unions, b) aggregate earning of BC credit unions, and c) many BC Crown corporations. For comparison, Coast Capital Savings Credit Union reported C$58 million net income in the year to December 2016. In the same period, BC credit unions collectively reported net income of C$263 million. Over recent years then net income of CUDIC relative to that of BC credit unions has increased materially, from 13% to 22%, principally due to material increases in deposit insurance premiums. Investment returns from the CUDIC deposit insurance portfolio funds FICOM operations.

The size of CUDIC assets may warrant it being a standalone organization. Between December 2007 and 2017, CUDIC assets increased from C$230 to C$596 million (Source: CUDIC). CUDIC assets have grown materially through higher system deposits, elevated funding policy target and fund transfer.

The B.C. Ministry of Finance should revisit its seeming business case for FICOM’s expansive mandate scope and instead prioritize effective structure, functional excellence and public accountability. The BC Ministry of Finance should strive to identify, and to adopt, best practices in regards the regulatory structures for credit unions. With the exception of BC then most, if not all, regulatory structures in other Canadian provinces separate regulatory functions into multiple organizations. Typically, regulatory policy and statutory approvals are performed by a provincial government organization, while deposit insurance and prudential supervision are executed by a provincial crown corporation (commonly a ‘Credit Union Deposit Guarantee Corporation’).

CUDIC prudential supervision may enable a simple, transparent funding model. The B.C. credit union industry would directly fund the majority of regulatory costs, including prudential supervision activities, through deposit insurance premiums to CUDIC, while the B.C. Ministry of Finance and/or stakeholders would fund residual FICOM functions. Most, if not all, monetary transfers between CUDIC and FICOM, and between FICOM and the BC Ministry of Finance, would terminate. The current funding model may be needlessly complex and appears significantly different from practices in other provinces.

“The B.C. Ministry of Finance should revisit it seeming business case for FICOM’s expansive mandate scope and instead prioritize effective infrastructure, functional excellence and public accountability.”

Legal separation between FICOM and CUDIC may be beneficial to government, industry, taxpayers and employees. The competency matrix, staffing requirements and labour market rates across the regulatory functions likely vary materially. There may be some functions that are performed to a higher standard; with greater timeliness; or on a cost-effective basis by public servants employed by the B.C. Ministry of Finance. For example, public servant direct access to B.C. government resources may provide clarity of discussions towards better and/or more timely decisions for statutory approvals. B.C. Ministry of Finance may seek to have direct input - perhaps to partly mitigate its deposit insurance risk - into processes that introduce, edit, or alter the intensity of regulatory policies. Employees may benefit from legal separation of FICOM and CUDIC as some current FICOM employees may prefer to remain in the public service.

Risk assessment responsibility and related funding source were significantly migrated from industry to government. In 2005, the relationship between FICOM/CUDIC and Stabilization Central Credit Union (‘SCCU’) - an entity owned and governed by B.C. credit unions - was significantly revised and “this resulted in the Stabilization Fund being reduced by $83 million to approximately $30 million, with the CUDIC deposit insurance fund increased by a like amount.” (Source: SCCU 2005 Annual Report). “These new arrangements restrict the flow of information between Stabilization Central and FICOM/CUDIC, with the result that Stabilization Central’s role in assessing risk is more limited” (Source: SCCU 2005 Annual Report). The 2005 fund $83m transfer was transformative in size relative to then asset sizes of CUDIC and SCCU.

SCCU should be considered as part of any regulatory restructuring. SCCU has a legislative mandate to act as the stabilization authority to B.C. credit unions. SCCU - owned, governed and operated by industry - appears to provide a valuable force for betterment in the credit union system. It advises specific credit unions that voluntarily choose, or have been required by FICOM, to initiate organizational changes. It promotes best practices across B.C. credit unions. In an environment of increased complexity and elevated regulations then it may act as an informed, cost-effective and trusted counsellor to boards of directors of B.C. credit unions - especially those of small and medium size. Its role contributes to the mitigation of deposit insurance risk. Annual reports of, and the 2015 FIA/CUIA submission by, SCCU disclose deliberations by its board in regards organizational viability and potential merger partners. They also highlight significant desire for a clearly defined, appropriately informed and credibly sustainable role. SCCU could play various future roles. Its functional responsibilities could be extended. Its legal status could remain as a standalone entity or be merged with Central 1 Credit Union or CUDIC. This submission does not consider related matters or propose specific recomendation(s). The B.C. Ministry of Finance should collaborate with industry to critically assess the business case, alternative strategic options, and effective future role of SCCU.

RECOMMENDATION 3 - LEADERSHIP & GOVERNANCE

Recommendation: Appoint permanent executive and an independent, empowered governance body to provide leadership and oversight of CUDIC. Related competency matrices and governance processes should reflect CUDIC financial size, technical complexity and systemic role. CUDIC Board should adopt, and strive for excellence in, relevant governance best practices.

By virtue of legacy legislation, CUDIC has never had dedicated executive leadership. The Superintendent of Financial Institutions also holds the official capacities of Superintendent of Pensions, Registrar of Mortgage Brokers, Superintendent of Real Estate plus CUDIC Chief Executive Officer. The CUDIC Executive Director, and limited CUDIC staff members, are FICOM employees. FICOM completes executive functions, such as establishment of the deposit insurance fund target policy, on behalf of CUDIC (Source: CUDIC annual report). FICOM staff provide significant operational services and administrative support to CUDIC.

For over two years, FICOM absence of permanent executive leadership has impacted CUDIC. Carolyn Rogers resigned as Superintendent of Financial Institutions in May 2016. Jeffrey Wu, Executive Director CUDIC, left FICOM at a similar date. Since that time FICOM has been led by an Acting Superintendent, Acting Superintendent Regulation, Acting Deputy Superintendent Prudential Supervision and Acting Deputy Superintendent Market Conduct. FICOM corporate functions are directed by an Interim CEO. Day to day operations of CUDIC are overseen by a FICOM employee that was appointed Acting Executive Director CUDIC.

CUDIC deserves full-time, permanent executive leadership:

its organizational size is larger than most B.C. credit unions and most B.C. crown corporations

its operating environment - the B.C. credit union industry - has increased materially in terms of size and complexity

its impact on supervisory risk assessments, and potential remedial interventions, to B.C. credit unions may be significant

its leadership competency matrix - including technical expertise, management skills and stakeholder relationships - may differ significantly from that required to set regulatory policy or assess statutory approvals

its responsibilities and resources, subject to above recommendations, may increase materially

By virtue of legacy legislation, CUDIC has never had dedicated governance oversight. Members of the FICOM Commission also act as Board Directors of CUDIC. As at March 2018, there were six appointed members of the FICOM Commission. It may be indicative of the conjoined relationship, of limited resourcing and/or of perceived functional priorities that CUDIC appears not to have submitted a response to the 2015 Initial Public Consultation Process of the FIA / CUIA consultation review. Were this the case then its Board of Directors should justify why CUDIC elected not to offer thought leadership, policy opinion and/or regulatory input on legislative matters at the core of its organizational purpose.

CUDIC Board may have mismatched competencies. Conjoined governance of FICOM and CUDIC implicitly requires compromise in appointee selection. Competency matrices are commonly used by a Board of Directors to balance its collective professional experience, environmental or contextual knowledge and personal attributes and skills. FICOM provides regulatory oversight for multiple industries including credit unions, insurance, trusts, pensions, real estate and mortgage brokers. FICOM Commission members presumably have appropriate expertise and experience across these industries, and understanding of related regulatory issues. Implicitly then only a subset of that expertise, experience and skills are relevant to credit unions and to CUDIC. Yet the CUDIC Board and FICOM Commission have identical membership.

Diverse conflict of interest requirements may limit the candidate pool for CUDIC Board. The Board Resourcing and Development Office related posting stated that “to be considered as a [FICOM] Commission member an individual must not have any real or perceived conflict of interest with the industries or institutions regulated by FICOM.” The conjoined governance structure therefore means that a candidate with a potential conflict of interest in the pension, mortgage broker, insurance or real estate industry is automatically prohibited from providing governance oversight of CUDIC and its credit union mandate.

CUDIC has outgrown legacy legislation and FICOM’s shadow. The size, complexity and impact of the B.C. financial services industry is material. Largely devised in the late 1980s then legacy legislation in regards leadership and governance of CUDIC may be outdated. CUDIC is responsible for deposit insurance of a C$77 billion industry that is used by almost half of British Columbians. Larger than most Canadian credit unions then it warrants full-time, permanent executive leadership. Larger than most B.C. Crown Corporations then it deserves independent, empowered and accountable governance oversight.

CUDIC Board should have the authority - and the resultant responsibility - to appoint and to assess its Chief Executive Officer and to develop executive compensation plans. Multiple governance experts identify CEO selection as a key function:

‘Selecting the chief executive officer and planning for CEO succession are among the most important responsibilities of a company’s board of directors.’ - Harvard Law School Forum for Corporate Governance & Financial Regulation ‘Advice for boards in CEO Selection and Succession Planning’

‘Choosing the next CEO is the single most important decision a board of directors will make.’ - Harvard Business Review, ‘The Art and Science of Finding the Right CEO’

‘During a CEO search process, boards might do well to keep their long knives sheathed because, in fact, real leaders are threatening to those intent on preserving the status quo’ - Harvard Business Review, ‘Don’t Hire the Wrong CEO’

CUDIC Board should demonstrate leadership to credit unions through its compliance with governance best practices.

RECOMMENDATION 4 - PUBLIC ACCOUNTABILITY

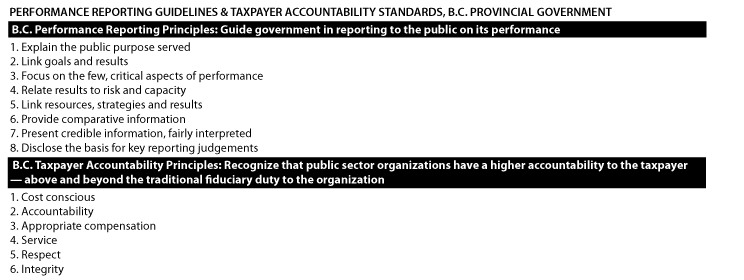

Recommendation: Regardless of their legal entity structure then FICOM and CUDIC should, as separate organizations, be subject to the “Performance Reporting Principles” and “Taxpayer Accountability Principles” as published by the B.C. government.

“Political accountability is the accountability of the government, civil servants and politicians to the public and to legislative bodies”

Governance bodies that oversee public service organizations are typically obligated to publish service plans, annual reports and other documents to public stakeholders. Disclosures may be driven by legislative requirement, government expectations or voluntary engagement.

Substantially all Canadian financial regulatory agencies appear to make extensive public disclosures. For example, Credit Union Deposit Guarantee Corporation - typically responsible for deposit insurance and prudential supervision functions in peer provinces - publish annual reports that are comparable to a public company. Such reports may contain some or all of audited financial statements; management discussion and analysis; CEO and Board reports; executive team profiles; governance practices; industry developments; regulatory updates; supervisory performance metrics; and/or executive compensation.

Public disclosures by FICOM and/or CUDIC appear to be negligible. Neither FICOM nor CUDIC publish an annual report or similar document that provides insight and rationale into goals, achievements, risks, key decisions, financial performance and/or other information. CUDIC publishes limited annual financial statements. As a ministry branch, FICOM disclosures could potentially be provided in the service plans and other reports published by the B.C. Ministry of Finance. But the most current Annual Service Plan Report (2015-2016) published by B.C. Ministry makes no reference whatsoever in regards financial statements, performance metrics or any other information for either FICOM or CUDIC.

Regardless of their legal entity structure, both CUDIC and FICOM should initiate compliance with the B.C. Performance Reporting Principles. In 2003, the B.C. government established “Performance Reporting Principles For the British Columbia Public Sector”. The related publication frames eight principles of deemed best practice that were approved by the Auditor General of B.C. The principles seek to support an open and accountable government.

FICOM should dislose, and provide credible rationale, to industry and to the public its plan to achieve key organizational goals. For example, the 2018/19 to 2020/21 Service Plan of the B.C. Ministry of Finance establishes a performance target for FICOM that, in 2017/18, 85% of financial institutions have a supervisory assessment completed in the prior three years.

In June 2014 “Taxpayers Accountability Principles”, the B.C. government introduced a new expectation “for deputy ministers ... to hold the entity [B.C. public service organization] accountable for the outcomes and measurements identified by the minister responsible, in consultation with the respective board chair.”

Executive leadership is obligated to make difficult decisions. This is the case in industry, government and communities. Some decision may involve topics that have high complexity, elevated sensitivity, material implications, accelerated timeline and/or significant subjectivity. Decisions may impact the organization, employees, communities and other stakeholders. Decisions may be made with imperfect information, unknown external forces and without the benefit of hindsight. Regardless, executive leadership and related governance body should be accountable to stakeholders for the resulting outcomes.

“The Taxpayer Accountability Princples state that ‘Board members act independently from the organization’s executive and have the best interests of taxpayers and shareholder as their primary consideration.’”

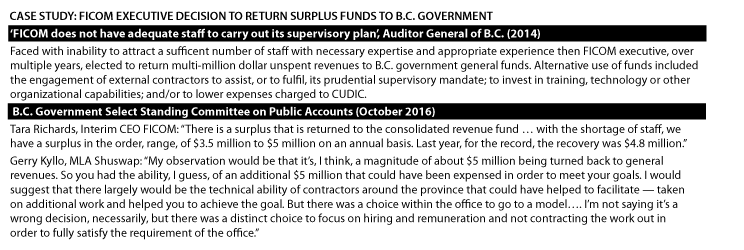

For example, FICOM executive and governance body should be accountable for decisions to return millions of dollars to B.C. general revenues rather than spend it on mandate fulfilment and/or operational betterment. Related funds were ultimately sourced from credit union deposit insurance premiums. Gerry Kyllo, MLA, neatly captured the situation in a Select Standing Committee - observing that FICOM executive faced multiple options and, regardless of whether “it’s a wrong decision”, a distinct choice was made. That such disclosures result from adhoc testimony to public officials rather than from routine stakeholder engagement processes may conflict with the intent of the Taxpayers Accountability Principles. Respectful of their primary consideration, FICOM Commission should routinely report to the public details of important goals, decisions and perfomance of FICOM and provide related rationale on how it perceives key aspects to reflect the best interests of taxpayers.

The funding basis and governance model of credit union regulation may be subject to a principal-agent gap. Despite industry funding FICOM/CUDIC operations then its contribution to related governance, and its receipt of perfoamnce disclosures, are both minimal and contary to practices in peer provinces. Lack of industry participation in oversight may have denied due challenge to FICOM Commission and executive. The 2015 submission to the FIA/CUIA consultation process by the B.C. credit union system noted that “as the funder of CUDIC, credit unions should have a greater voice in its governance.”

REFERENCES

Selected Deposit Insurance Organizations

CUDIC (BC) - http://www.cudicbc.ca

CUDGC (AB) - http://www.cudgc.ab.ca

CUDGC (SK) - https://www.cudgc.sk.ca/about-us/

DGCM (MB) - http://depositguarantee.mb.ca/home/

DICO (ON) - http://www.dico.com

CDIC (Federal) - https://www.cdic.ca

Stabilization Central Credit Union - https://www.stabil.com/

Government References

FICOM - Supervisory Framework - https://www.fic.gov.bc.ca/pdf/aboutus/FICOMSupervisoryFramework.pdf

B.C. Government - “Taxpayer Accountability Principles” - https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/services-policies-for-government/public-sector-management/taxpayer-accountability-principles.pdf

B.C. Government - “Performance Reporting Principles” - https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/services-policies-for-government/public-sector-management/performance_reporting_principles.pdf

BC Select Standing Committee on Public Accounts - Draft minutes, October 2016 - https://www.leg.bc.ca/documents-data/committees-transcripts/20161005am-PublicAccounts-Vancouver-Blues

B.C. Ministry of Finance - “2015/16 Annual Service Plan Report” - http://www.bcbudget.gov.bc.ca/Annual_Reports/2015_2016/pdf/ministry/fin.pdf

B.C. Ministry of Finance - “2018/19 – 2020/21 Service Plan” - http://bcbudget.gov.bc.ca/2018/sp/pdf/ministry/fin.pdf

Federal Department of Finance and Treasury Board of Canada - “Directors of crown corporations: an introductory guide to their roles and responsibilities” - http://publications.gc.ca/collections/collection_2016/fin/BT77-1-1993-eng.pdf

Statistics Canada - 2016 Census data - https://www12.statcan.gc.ca/census-recensement/2016/dp-pd/hlt-fst/pd-pl/Table.cfm

Sources Referenced in Submission

Canadian Credit Union Association - Top 100 Credit Unions, Q4 2017 - https://www.ccua.com/~/media/CCUA/About/facts_and_figures/documents/Largest%20100%20Credit%20Unions/top100-4Q17_12-Apr-18.pdf

Canadian Credit Union Association - System Results, Q4 2017 - https://www.ccua.com/~/media/CCUA/About/facts_and_figures/documents/Quarterly%20National%20System%20Results/4Q17SystemResults_14-Mar-18.pdf

Harvard Law School Forum on Corporate Governance and Financial Regulation, ‘Advice for boards in CEO Selection and Succession Planning’ - https://corpgov.law.harvard.edu/2012/06/11/advice-for-boards-in-ceo-selection-and-succession-planning/

Canadian Coalition for Good Governance - ‘Building High Performance Boards’ - https://www.ccgg.ca/site/ccgg/assets/pdf/building_high_performance_boards_august_2013_v12_formatted__sept._19,_2013_last_update_.pdf

McKinsey & Company - “The CEO Guide to Boards” - https://www.mckinsey.com/featured-insights/leadership/the-ceo-guide-to-boards

FIA/CUIA System Response - http://www.fin.gov.bc.ca/pld/files/BC%20Credit%20Union%20System%20Response.pdf

Wikipedia - Accountability - https://en.wikipedia.org/wiki/Accountability

DISCLAIMER & COPYRIGHT

This article reflects the personal recommendations and statements of the author, Ross McDonald. It is wholly intended to assist the B.C. Ministy of Finance as part of the FIA/CUIA Public Consultation. This article does not represent the views of any financial cooperative, corporate organization, regulatory body or government ministry. All content is wholly based on information that is in the public domain. Where relevant, sources have been identified and referenced.

Although the author has made significant effort to ensure that the information in this submission was accurate at the date of completion then the author does not assume any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.